BRB Bottomline: [this text is italicized but not bolded, copy and paste text only into the text box on the left to usually adjust formatting]

Investors are constantly encouraged to think long term. But how long is long?

Ten years? Twenty years?

What about three hundred?

That’s the vision of Masayoshi Son, the self-made 60-year-old billionaire founder and CEO of SoftBank, a massive Japanese mobile telecom and investment firm. Masa is betting $100 billion on a portfolio of 300-year-long moonshots with his (aptly named) Vision Fund. In this article, we’ll take a look at the Vision Fund—what it is and what it means for startups, venture capital, and everyday investors like you and me.

The Japanese Investor that Changed Venture Capital

After graduating from UC Berkeley in 1980, Masa went back to Japan and founded SoftBank, through which he rode the dot-com boom of the late nineties and invested billions into internet companies—at one point, he reportedly owned 25% of the Internet. Masa’s investment in Alibaba is often cited as the single greatest investment in history, turning an initial $20 million into about $120 billion today.

It hasn’t been all sunshine and rainbows, though. When the dot-com bubble burst in 2000, Masa’s net worth reportedly dropped by $70 billion. On the David Rubenstein Show, he talks about what it feels like to lose more money than any person who has ever lived; it’s an insightful interview.

Still, Masa hasn’t shied away from making big bets. Cue the Vision Fund.

Vision Fund: Just the First $100 Billion

The Vision Fund is all part of Masa’s 300-year vision for SoftBank—and the world. It’s an investment fund with $100 billion which will make investments primarily focused on technology, especially artificial intelligence.

Masa’s plan for the Vision Fund is to take large positions in companies that he believes will change the world and, in doing so, generate commensurate returns. Already, it has significant stakes in Uber, WeWork, and GM Cruise, an autonomous vehicle company bought by General Motors. And Masa is just getting started. He plans on raising more of these $100 billion funds, investing about $50 billion a year. In comparison, the entire U.S. venture capital industry spent $75.3 billion in 2016; globally, VC firms raised only $64 billion and spent just over $100 billion.

Some critics contend that Masa’s investments are haphazard, but he argues that there’s a common thread: “I have shifted entirely,” Masa has said, “so that I am devoting 97% of my time and brain on AI.”

Venture Capital: Feeling the Heat of the Son

SoftBank is based in Japan, but Masayoshi Son’s investments have far-reaching consequences around the globe. In the world of ride-hailing startups, SoftBank owns stakes in some of the biggest players in the U.S., China, Brazil, India, and Southeast Asia.

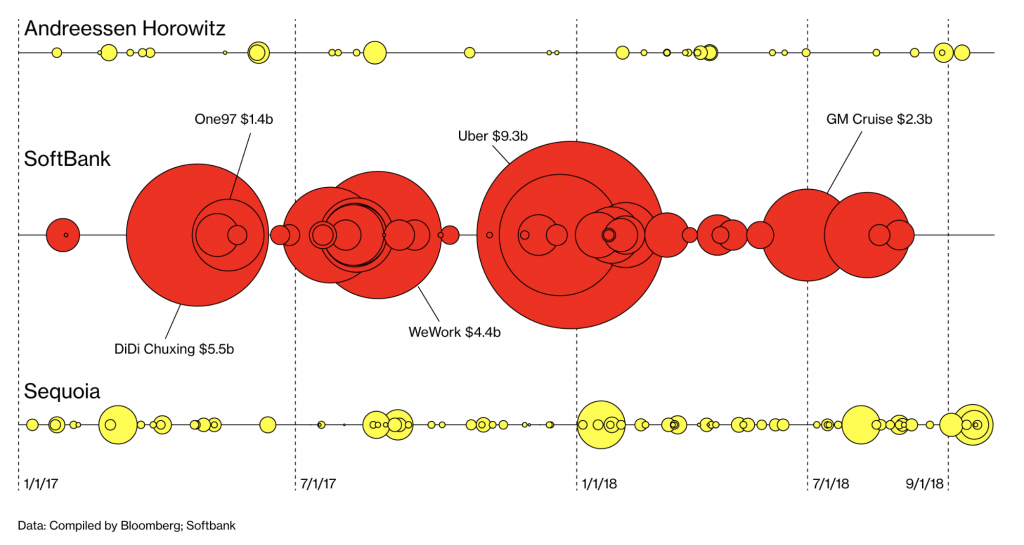

Perhaps the place where Masa’s investments have made the biggest impact is Sand Hill Road. Nestled in the heart of Silicon Valley, this 5.6-mile stretch of road has become synonymous with venture capital (VC). It’s home to VC heavyweights like Andreessen Horowitz and Sequoia Capital—and it’s just another industry Masa is disrupting.

The modus operandi for these VC firms is to start small: identify a promising startup, and give it a little money. As it grows, feed it more. Eventually, when the VC wants to liquidate its position (convert its stake in the company to cash), it puts its exit strategy into motion, usually through an initial public offering (offering shares on a public stock exchange) or by selling the company to another.

Masayoshi Son’s Vision Fund, though, is changing the game. Instead of successively larger funding rounds, Masa is adopting a different strategy: if you like a company, just throw money at it.

A lot of money.

The Vision Fund’s smallest investments are around $100 million. Its biggest? A $9.3 billion bet on Uber.

The numbers are astronomical, and the sheer size of SoftBank’s investments is putting traditional VC companies on edge. A partner at one firm reportedly referred to SoftBank as “a big stack bully,” a poker term used for a player with a dominantly huge stack of chips. For perspective, Sequoia Capital, one of the most prominent VC firms in Silicon Valley, has raised a total of only $14.6 billion. Andreessen Horowitz, another Sand Hill leader, has only raised $6.6 billion.

VC firms like Sequoia and Andreessen Horowitz have had little choice but to adapt to the competition. Sequoia is raising about $12 billion across various venture capital and growth funds, and Kleiner Perkins, another VC firm, is splitting into two in an effort to specialize in different stages of startup growth. That move reflects the rapidly changing VC landscape spurred on in part by the Vision Fund’s massive capital injections into both early- and late-stage startups.

Masa’s Biggest Backer is A Prince

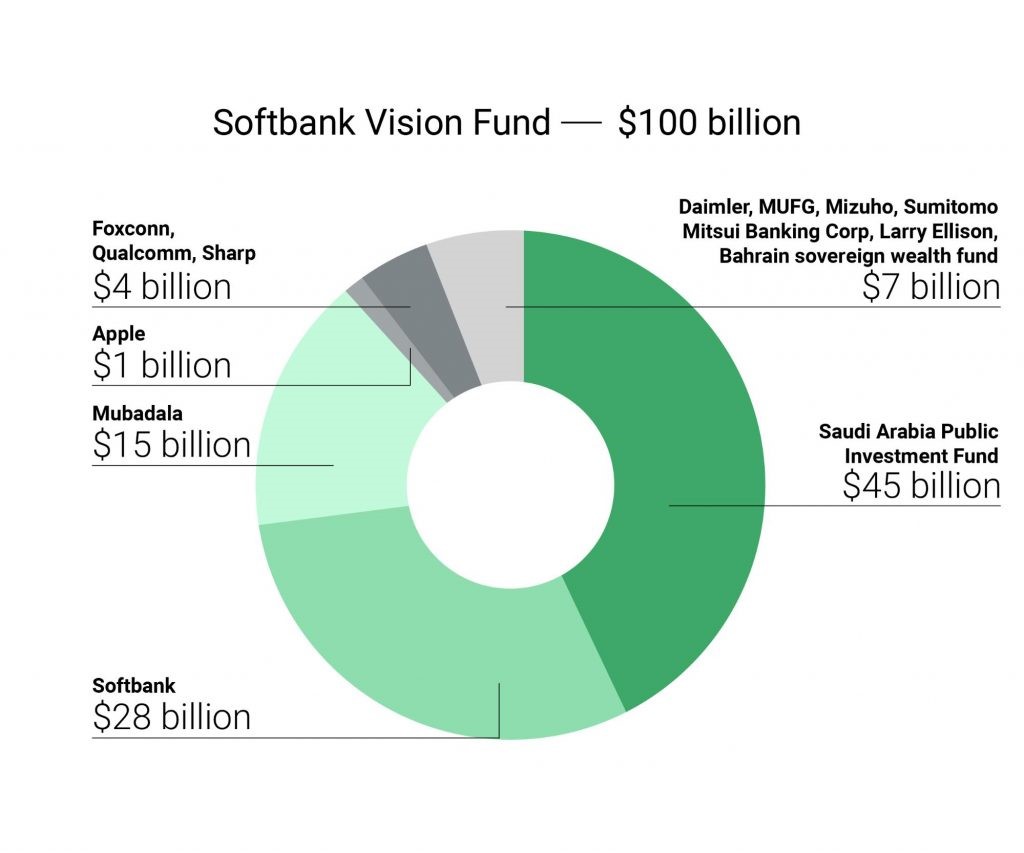

Only $28 billion of the $100 billion Vision Fund is SoftBank’s money. Where, then, did Masayoshi Son get the rest?

The largest piece is a $45 billion commitment by Saudi Arabia’s crown prince, Mohammed bin Salman, who sits over the kingdom’s Public Investment Fund. His support has attracted money from other investors, including $1 billion from Apple and $15 billion from a state-owned investment fund in Abu Dhabi. Foxconn, Sharp, and Qualcomm have joined in as well. The final $7 billion was offered by Mercedes Benz car-maker Daimler, along with three Japanese banks, Oracle co-founder Larry Ellison, and Bahrain’s sovereign wealth fund.

The Vision Fund certainly comprises an eclectic mix of investors, from billionaires to corporations and sovereign wealth funds, but it’s Saudi Arabia’s commitment that stands out particularly.

Saudi Arabia’s contribution comes out of its Public Investment Fund, or PIF. Established in 1971, the PIF is central to Vision 2030, the kingdom’s plan to diversify its oil-dependent economy. Its assets add up to about $230 billion, and it has many other investments outside the Vision Fund, including an almost 5% stake in Tesla and a $20 billion investment in a U.S. infrastructure fund run by Blackstone Group LP.

The PIF was key to Masa’s first Vision Fund, and it could be what makes a second one possible. In an interview with Bloomberg earlier this year, Prince Mohammed expressed interest in committing another $45 billion to Masa’s second Vision Fund, bringing the PIF’s total contribution to $90 billion across the two funds. It’s no wonder why: according to Masa, the Vision Fund returned over 20 percent in its first five months.

But Saudi Arabia’s central role in the Vision Fund has raised some tough geopolitical questions. After the mysterious disappearance of journalist Jamal Khashoggi in early October, politicians and business leaders around the globe have mounted backlash against the Crown Prince and other Saudis accused of orchestrating his death—with huge financial consequences.

SoftBank’s share price fell from a near-high of $100.36 on the date of Khashoggi’s disappearance (October 2) to $73.95 almost four weeks later. The 26% drop is likely due in large part to the uncertainty raised by Khashoggi’s apparent murder. As Amir Anvarzadeh, a strategist at Asymmetric Advisors, noted, companies might turn down a Vision Fund investment to avoid being “associated with what they might consider as blood money.” After all, if you’re the CEO of a Silicon Valley darling, do you really want to take the money of a country accused of murdering a journalist?

This could jeopardize Masa’s dream of Vision Fund 2 as well. The fund’s dependence on the Saudis “might chase some people from the fund,” according to Dan Baker, senior equity analyst with Morningstar. A joint investment with Saudi Arabia exposes other Vision Fund investors to risks arising from potential geopolitical conflicts—and those are risks many might not be willing to take on.

Still, Masa Has Permanently Changed VC

Even if Vision Fund 2 never takes off, the first will undoubtedly have lasting repercussions.

For one, the sheer size of the Vision Fund concentrates enormous power in the hands of just a few men. Being a “big stack bully” means Masayoshi Son can push out competition from other VC firms, offering startups millions, even billions, more than the competition can. It also means that Masa and his team are essentially hand-selecting which companies will succeed in their industries; after all, an infusion of hundreds of millions of dollars from the Vision Fund is a massive leg up over competitors.

This consolidation of power gives SoftBank the ability to position its portfolio companies to compete effectively—or, in some cases, not to compete against each other at all. Take ride-hailing for example: SoftBank owns large stakes in numerous ride-hailing companies, including Uber and Grab. Not wanting to see Uber bleed money competing with another one of SoftBank’s portfolio companies, SoftBank pushed Uber to sell its Southeast Asia business to competitor Grab, in which SoftBank has invested almost $4 billion. By carving out geographies for each of its ride-hailing companies, SoftBank can prevent them from driving down each other’s prices the same way Lyft and Uber have done to each other in many U.S. cities.

To be sure, Masa doesn’t have the power to completely reroute global competition, and holding interests in multiple competitors does risk cannibalizing the company’s own profits. Didi, a SoftBank-backed Chinese ride-hailing company, intends to make a push into Japan soon—a market in which Uber also intends to compete.

Another repercussion of the Vision Fund is that billions of dollars in private money have flooded into late-stage startups, precisely at the point when startups historically turned to public markets for cash. There’s a broad trend now of startups choosing to stay private longer, only IPOing when founders or early investors want liquidity for their shares. Some unicorns (billion-dollar startups) do end up choosing to IPO, like Spotify or MongoDB, but these instances are becoming rarer as staying private becomes a more alluring option. Private companies are not beholden to the same short-term profit-minded shareholders that public companies are, nor do they have to report quarterly earnings or prepare the same long financial reports.

A bullish (optimistic) observer would argue that because companies have more leeway with private investors than public ones, they can play more of a long game, focusing on long term growth rather than giving in to short term profitability demands. This is especially useful for companies dependent on demand-side economies of scale, also called the network effect—terms which refer to when products become more useful as more people use them. Uber, for instance, only has value if there are enough of both drivers and riders. It takes time for companies to reach this critical mass, and private funding allows them the flexibility to grow, away from the public spotlight.

A bearish (pessimistic) observer would instead contend that this level of private funding is utterly unsustainable. The valuations for these companies (many of which have yet to turn a profit) are massive, and some would say that without public scrutiny, many have become wildly overvalued, especially over the course of many successive fundraising rounds. If and when these companies do go public, many are brought back down to earth—just take a look at the stock price of Snap.

There’s another major consequence of the increase in private capital: at a very basic level, companies delaying IPOs means they’re not on the public markets, so everyday investors like you and me can’t own their shares and thus can’t partake in their profits. Theoretically, if this trend continues on a large enough scale, it could exacerbate the rising wealth inequality facing our country. This gap is the widest it has ever been, and with Masa and SoftBank keeping private companies private, the wealth gap between wealthy investors and regular retirees could widen even more.

When it Comes to Disruption, Wall Street Joins Sand Hill Road

Venture capital and retail investors aren’t the only ones affected by the Vision Fund and this broader stay-private-longer trend. Investment banks could also take a hit, as startups find it increasingly unnecessary to tap the connections that they’ve traditionally sold access to.

Underwriting IPOs, after all, makes up a significant portion of an investment bank’s revenues. (Underwriting, in this context, is when the investment bank commits to selling a certain amount of a company’s stock to institutional investors in the IPO process. You can read more here.) Equity underwriting, which includes both initial public offerings and follow-on offerings, made up $1.5 billion out of $5.5 billion of Morgan Stanley’s investment banking revenue in 2017. The underwriters for Alibaba’s IPO in 2014—Citigroup, Credit Suisse, Deutsche Bank, Goldman Sachs, JPMorgan Chase, and Morgan Stanley—earned over $300 million in fees from that deal alone.

Though equity underwriting fees for U.S. investment banks recovered to $6.1 billion in 2017 after a 2016 slump, that’s still below the $6.4 billion per year average of the last ten years. And though these underwriting fees are rising globally, U.S. banks have experienced a sharp decline in their share of the pie.

Sure, you might not feel sorry for ultra-rich Wall Street bankers, but their profitability affects you, too. Wealth management—when an investment bank manages your money and charges fees for various services—also makes up an important portion of bank revenue. If the IPO market cools in the coming years, there’s a possibility that investment banks might try to raise your fees to make up the difference in lost underwriting revenue.

Take Home Points

In the end, Masayoshi Son’s Vision Fund isn’t just about one man’s dreams. It’s a story about the future of venture capital. Of geopolitics. Of investment banking. Of wealth inequality, even. It’s a story about looking ahead into the ultra-long term.

Is the Vision Fund model of enormous bets on hotshot entrepreneurs sustainable, or even profitable? It’s doing well so far. In the first quarter of 2018, SoftBank reported a 60% increase in operating profit over the same time a year ago, bolstered by a ¥65 billion contribution (almost $600 million) by the Vision Fund.

Still, it’s a bit too early to say for sure. Instead, we can all learn a little from the long-term mentality of a man with a vision—better, a Vision Fund.

You completed a few nice points there. I did a search on the theme and found nearly all persons will consent with your blog.

I keep listening to the news update speak about getting free online grant applications so I have been looking around for the best site to get one. Could you advise me please, where could i acquire some?

Thanks for another informative blog. The place else could I get that kind of information written in such a perfect means? I’ve a project that I’m simply now working on, and I’ve been on the glance out for such info.

Good ¡V I should certainly pronounce, impressed with your website. I had no trouble navigating through all the tabs as well as related information ended up being truly simple to do to access. I recently found what I hoped for before you know it in the least. Quite unusual. Is likely to appreciate it for those who add forums or anything, website theme . a tones way for your customer to communicate. Excellent task..

you are actually a good webmaster. The website loading velocity is amazing. It seems that you are doing any distinctive trick. In addition, The contents are masterpiece. you’ve done a excellent process on this subject!

Howdy very cool site!! Man .. Excellent .. Wonderful .. I’ll bookmark your web site and take the feeds also¡KI am glad to search out numerous useful info here within the post, we want work out extra strategies on this regard, thanks for sharing. . . . . .

Thank you so much for giving everyone an extraordinarily special opportunity to read critical reviews from this site. It’s always very enjoyable and jam-packed with amusement for me and my office colleagues to search your web site a minimum of thrice in a week to see the newest tips you have. And definitely, we are at all times amazed with all the wonderful tactics you give. Selected 1 areas in this post are particularly the finest we have all had.

I am constantly searching online for ideas that can facilitate me. Thanks!

Hello.This post was extremely interesting, particularly because I was looking for thoughts on this topic last Thursday.

Thanks for another informative blog. The place else could I get that kind of information written in such a perfect means? I’ve a project that I’m simply now working on, and I’ve been on the glance out for such info.

Hello.This post was extremely interesting, particularly because I was looking for thoughts on this topic last Thursday.

Great post. I was checking continuously this weblog and I’m inspired!

Extremely helpful info specially the remaining section 🙂 I care

for such info much. I used to be seeking this particular info for a long

time. Thank you and best of luck.

I simply wanted to thank you so much again. I am not sure the things that I might have gone through without the type of hints revealed by you regarding that situation.