Author: Vardaan Tekriwal, Graphics: Osayd Asif Bashir

The BRB Bottomline:

Instead of the common demand-pull inflation, the global economy seems to be facing its unfavorable counterpart, stagflation. However, instead of waiting out its transience, central banks globally are continuing to enforce contractionary monetary policy. Learn more about the trade-offs that hiking interest rates has on the local and global economy.

The Current Economic Landscape

Several central banks around the world have yet again demonstrated their commitment to curb inflation by raising interest rates. The United States Federal Reserve hiked the cost of borrowing by 75 basis points for the fourth consecutive time this year, amounting to a cumulative increase of 3%. After the Fed’s third increase, other major economies, including India and South Korea, followed suit, increasing their interest rates as well. Though these decisions to hike interest rates should have positive effects in cooling down inflation, they may — perhaps counterintuitively — achieve the opposite of what was intended.

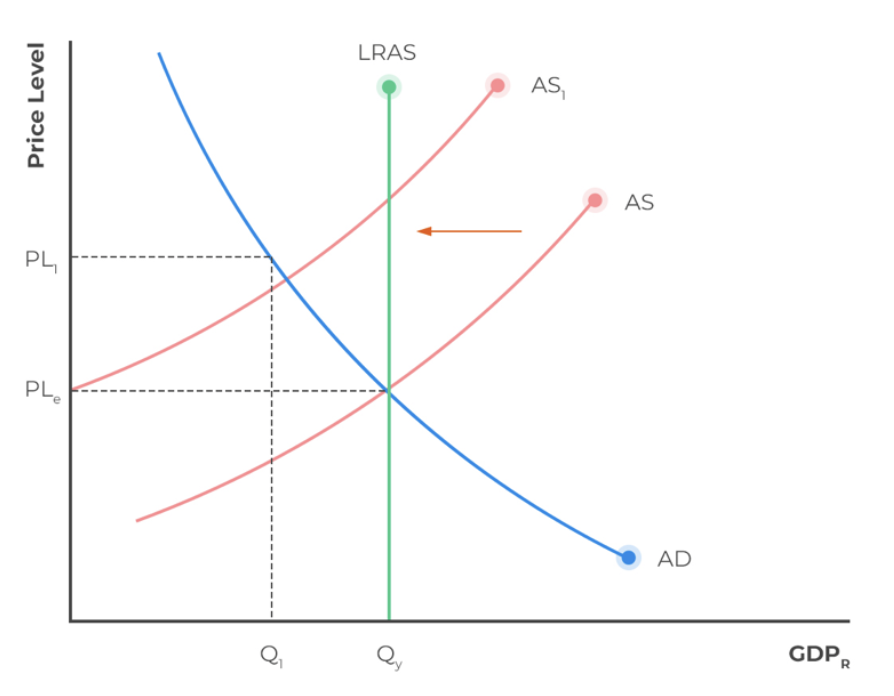

Several key developments in the global landscape have contributed toward the current inflationary situation. These developments include the Russo-Ukrainian war and adverse environmental impacts in South America and Southeast Asia, which have affected commodity yields and thus supply chains. Energy prices, shipping costs, and commodity prices have all seen a sharp increase, resulting in a burst of cost-push inflation. This type of inflation, illustrated in Figure 1, is also known as stagflation.

The figure above illustrates a market experiencing

cost-push inflation, also known as stagflation.

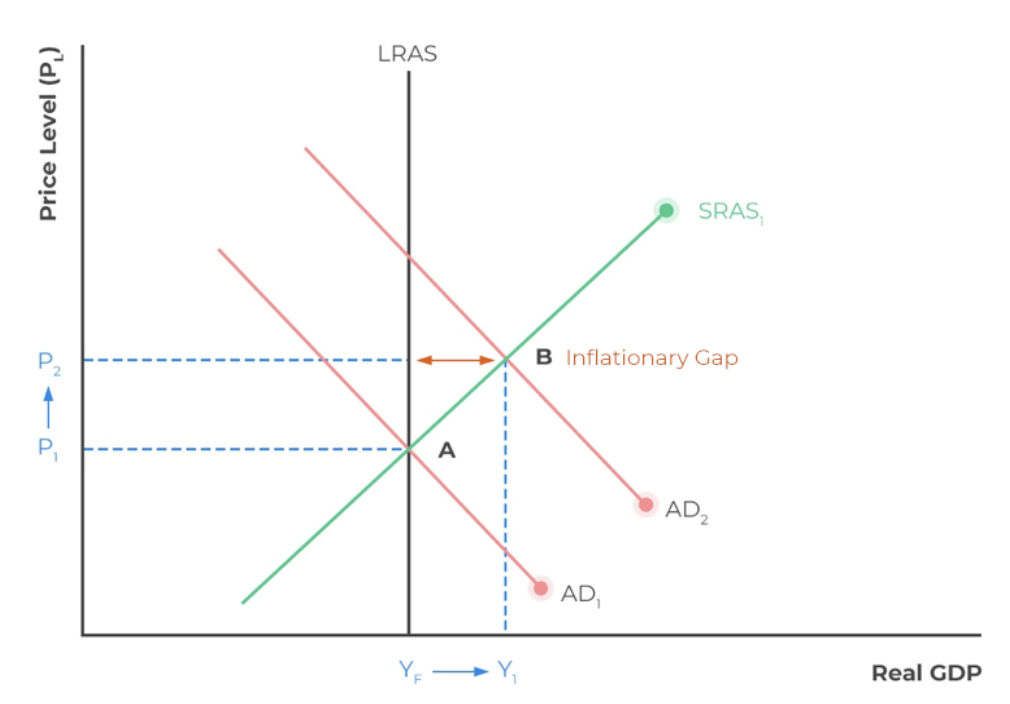

Furthermore, a more common cause of inflation, an increase in consumer demand, has also impacted the economy. The recent unprecedented increase in the demand for consumer goods and services, in the wake of the COVID-19 pandemic, has driven up the Consumer Price Index (CPI), a metric that measures the change in prices for everyday products over time. This increase translated to excess demand, and resulted in demand-pull inflation — the usual cause of inflation (Figure 2).

The figure above depicts a market experiencing

demand-pull inflation.

These two types of inflation, cost-push and demand-pull, should be acted upon independently. In other words, policy intended to curb inflation should be specifically targeting cost-push or demand-pull inflation, without conflating one for the other.

Macroeconomic theory suggests that without any outside intervention, the macroeconomy will self-adjust and return to its long-run state after short-term shocks. The decision for policymakers thus boils down to a cost-benefit analysis taking into account factors like intertemporality and risk tolerance — they can either wait and allow the economy to adjust organically, or sink resources into actively trying to stabilize the economy, taking on the risk of further destabilizing it. In the case of raising interest rates in order to reduce inflation, policymakers run the risk of overtightening, dragging the economy into a recession.

Cost-Push vs. Demand Pull

Cost-push inflation is normally transient; in other words, it takes less time to achieve “long-run” adjustment than does demand-pull inflation. An example is the U.K. economy during the Great Recession. However, cost-push inflation has a greater impact on the community, since the price of goods increases without any consumer-side change, so people are required to spend more of their real wealth. On the other hand, demand-pull generally takes more time to resolve — which is why it could warrant monetary policy — and has a lesser effect on the general population. An increase in disposable income is normally the driver for increased consumerism, so while the price of goods are rising, consumers’ incomes are rising as well.

Therefore, the Federal Reserve increasing interest rates — a method of contractionary monetary policy primarily used to tackle demand-pull inflation — demonstrates that they are weighing the rise in demand more than the accumulation of rising supply-side costs.

Central Banks’ Justification

In the long term, the increase in interest rates contracts the economy; it discourages borrowing and financing, thereby directly reducing overall investing ceteris paribus, leading to a decline in GDP. Discouraging investing (i.e., capital expenditure), eliminates its intrinsic benefit in stimulating financially sustainable growth through expanding the production possibilities frontier.

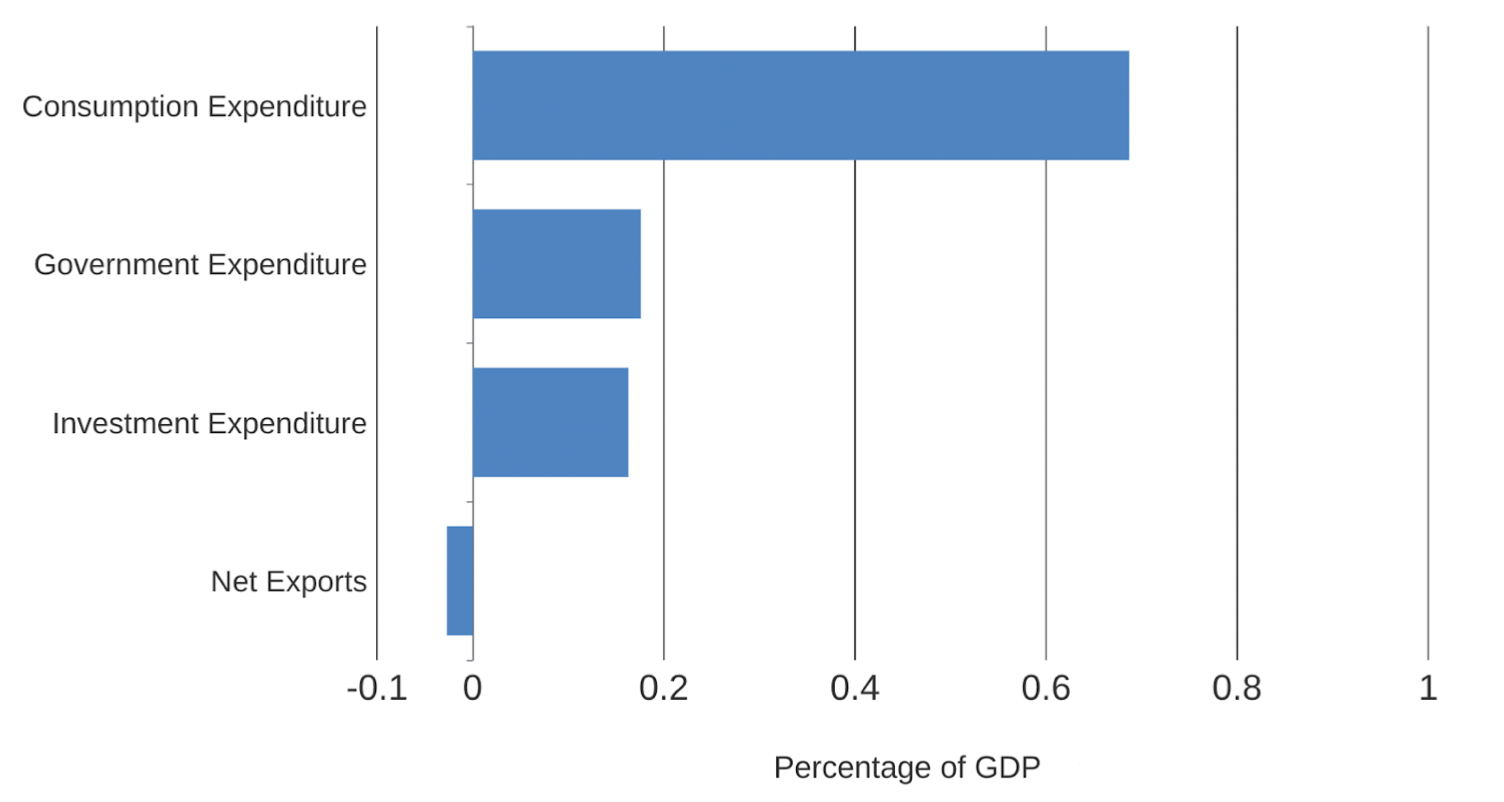

The justification for enforcing this decision, then, is that it protects consumers in the short run. The pandemic, among other factors, has had grave impacts on the public’s disposable income. Hence, with consumer spending constituting over two-thirds of the United States’ GDP, as shown in Figure 3, it is of great importance to take measures to bolster private consumption expenditure.

The bar chart breaks down the constituents of

the United States’ GDP. Note that ‘Net Exports’

subtracts from the GDP.

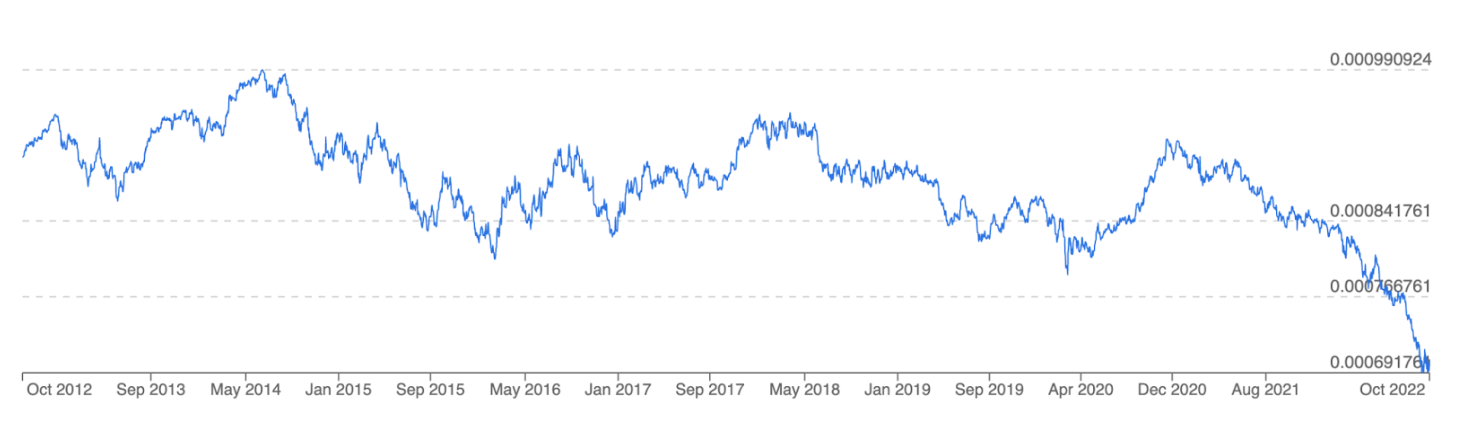

The United States’ increase in their interest rates is reflected in the changes of global economies as well. This contractionary monetary policy appreciates the value of the US dollar on the foreign exchange market. The Indian rupee and South Korean won are weakening against the dollar, breaking their ten-year lows, while the two countries’ central banks have also hiked their interest rates up by 50 basis points each.

The weakening of local currencies of export-based countries does mean that they are incentivized to export more, because goods manufactured with their local currencies are denominated in stronger currencies. In theory, this should stimulate economic growth. However, India and South Korea, who are grappling with the same global macro phenomena that the United States is, undergo similar justifications of weighing demand-pull inflation over cost-push.

The time series chart illustrates the exchange of

INR to USD. The data and graph are provided by

the XE Currency Converter.

The time series chart illustrates the exchange of

KRW to USD. The data and graph are provided by

the XE Currency Converter.

Conclusion

The priority of central banks around the world is to protect the consumer. Their monetary policies aim to sustain the increased demand that the end of the pandemic is bringing. On the other side of the macroeconomy, when supply-side costs decrease, the pieces should come together — a healthy consumer market will once again become the driver for holistic, sustained economic growth.

Take-Home Points

- Several central banks around the world have yet again are attempting to curb inflation by raising interest rates.

- The current macroeconomic environment creates the exigency for significant trade-offs.

- Central banks worldwide are prioritizing short-term stability at the expense of sustained, long-term growth.

- When supply-side costs decrease, a healthy consumer market will contribute to sustained economic growth.